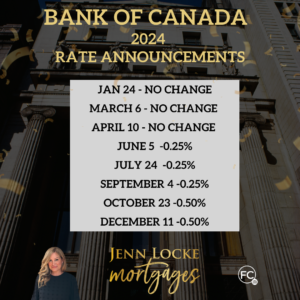

This last Bank of Canada rate announcement of 2024 gives us another 0.50% cut to the central bank rate bringing it to 3.25% which is at the top-end of a neutral rate. Most mortgage lenders will now have a Prime lending rate of 5.45%. It is important to note that while we see 3.25% in the news, we generally have to add 2.2% and that’s the Prime lending rate that affects Variable rate mortgages.

To put it simply, 3.25% is now the rate that banks/lenders can borrow money. They then add 2.2% to it to determine Prime (now 5.45%) and they either attach a discount or a premium to Prime to determine the effective lending rate for variable rate mortgages or home equity lines of credit. Some banks add more than 2.2% and have higher Prime lending rates. I’m always happy to chat more in detail about this as it can be confusing.

Since June 2024, Prime has come down by 1.75% from 7.2% to 5.45%, which delivers some much-needed relief to Canadians. This impacts all forms of variable interest rates including credit cards and lines of credit.

For Adjustable Rate Mortgages (ARM), for every $100,000 owed, our payments decrease by approximately $13/month. Since June, we have seen the equivalent of seven (7) cuts of 0.25%. For a $500K mortgage, this translates into savings of approximately $455/mo. This is significant not only for those of us currently in an ARM or HELOC, but it also helps with qualification for new mortgages. Contact me if you have any questions about this.

It’s important to note that depending on when your next mortgage payment is scheduled for, you might not see this payment decrease until well into January. Don’t fear though, the savings in interest will be applied to your principal until your payments are adjusted.

What does this mean for you?

- Adjustable-rate mortgage holders: You’ll see a slight drop in your mortgage payments, giving you extra cash flow every month. (see above)

- First-time buyers: Lower rates mean increased borrowing power, making it a great time to find your dream home.

- Upcoming renewals: If your mortgage renewal is on the horizon, this lower rate could work in your favor and ease your financial planning.

- Possible interest savings strategies: If you are in a fixed rate mortgage over 5%, there could be an opportunity to make adjustments to your mortgage and save you money.

No matter your situation, this is positive news for Canadians nationwide. If you have any questions about how this rate change impacts your mortgage or plans, don’t hesitate to reach out—I’m here to help!

Now, for those of you who are more analytical and would like some of the headlines broken down, read on…

Why the second half-point cut in a row?

Simply put, it’s due to bad news in the economy. The sad reality is that bad economic news = good news for interest rates.

However, let’s start with the good news first. Inflation is hovering at the BoC’s target of 2%. If you remove mortgage interest from this number we are closer to 1.4%. There will always be ebbs and flows. For instance, Taylor Swift inflation is real! Hotels, restaurants etc. all increased prices in cities where she played. Google “Taylor Swift Inflation” and you’ll see headlines from the UK and Sweden… of course, this is temporary. I digress. Another temporary inflationary item in Canada is the pause on GST/HST from December 14, 2024 – February 15, 2025. The Bank of Canada understands these things will not have a long-term impact on inflation and still went ahead with the larger cut today.

Declining Productivity & Flat GDP

Canada currently has the second lowest measure of productivity growth of G7 countries, second to Italy. What’s more disturbing is that Canada’s GDP per capita is lower than all individual US States, with the exception of Mississippi. The BoC is paying close attention to GDP and the plans for restricted immigration will have a further adverse effect, according to Bank of Canada Governor Tiff Macklem.

Government Spending

Government spending is hugely inflationary and most of their spending is not investing in productivity, which is what we desperately need. Our Feds will be doling out handouts of $250 to all working Canadians and Ontario will be providing a $200 taxpayer rebate in 2025. This is an example of spending that is not investing in overall productivity, which will establish long-term benefits. Why not instead invest in healthcare, education or transportation ie) high speed rail routes between major and emerging city centres? In my humble opinion, one word comes to mind. Votes.

Government spending is outpacing GDP by a long shot. We have had 5 consecutive quarters of flat GDP growth at 2.1% while the Federal Government deficit growth is up 23%. The deficit is up from $11.9B in 2019 to $50.9B!

If it weren’t for profligate government spending, the BoC likely would have raised the key lending rate from 1.75% to around 3% but, they overshot and went to 5% (translating to a Prime rate of 7.2%) which has led to a lot of non-mortgage delinquencies this year.

Interest Payments, Insolvency Rates & Unemployment

Interest payments are eating up Canadians’ incomes more than since 1992 and we are now paying more than double the interest payments since 2019, pre-pandemic.

Insolvency for non-mortgage debt in Canada is up 13.5% in Q3 of this year vs the same time in 2023 and in Ontario it’s up by 20.2%. Business insolvencies are up 16.2% nationally and 40.2% in Ontario.

Furthermore, Property Development receiverships are on pace for a record year in 2024 with more construction and real estate insolvency filings ever…. All amidst a critical housing shortage. There is a massive disconnect here and we need fast-acting effective programs to correct this. Not Good.

Unemployment rate for November 2024 was measured at 6.8% which is the highest reading since September of 2021.

The Trump Threat

Headlines have shared with us that the Canadian Dollar is down to $0.70 from $0.73 since June, compared with every US $1 . The fact that the BoC still gave us a 0.50% cut signals that other factors are more pressing and the risk of a lower CAD dollar is not as important as countering other issues. In fact, the BoC views this rate cut as a form of insurance against Trump’s threat of a 25% tariff on Canadian goods – which is a major new uncertainty. I like to think he is in large part threatening this to strengthen his negotiation power, as this would be inflationary to the US as well. Time will tell.

How Low Will the Bank of Canada Go?

Well, in years of noteworthy economic crises & struggles, the average rate drop in the span of a 12 month period averages at 2.5%. This would indicate that Prime would be down to 4.70% by June 2025. Remember however, that the BoC overshot, bringing the central rate up to 5% (usually the emergency monetary tightening would be 3%) so this suggests the cuts are not likely to stop there.

I like to say that my crystal ball is on backorder, however it is fairly safe to say that more rate cuts are in store moving into 2025. How low? No one really knows, but in the 10 years between the recovery of the 2008 financial crisis and the start off the in 2020 pandemic, The Prime lending rate hovered between 2.70-3.95% (central bank rate hovered between 0.50-1.75%). There is definitely room to keep the cuts coming.

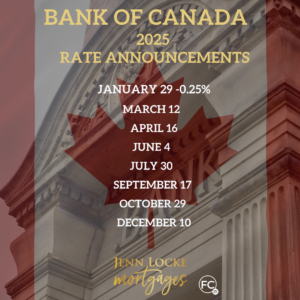

The next Bank of Canada rate announcement is scheduled for January 29, 2025 and I’ve attached the 2025 schedule for you here. Follow me on FB, IG and LinkedIn for ongoing updates and tips at @jennlockemortgages.

As always, if you have any questions about how this affect you or anyone you know, please contact me and/or share my information. I’m always happy to have a chat and help in any way I can.

Leading up to the holidays, I wish you all a wonderful season of making memories with loved ones.

My very best,

Jenn